Structural Changes in the Digital Ad Market and Opportunities for 2023

Structural Changes in the Digital Ad Market and Opportunities for 2023

A Space Undergoing Fragmentation, with New Products and Challengers Gaining Marketshare

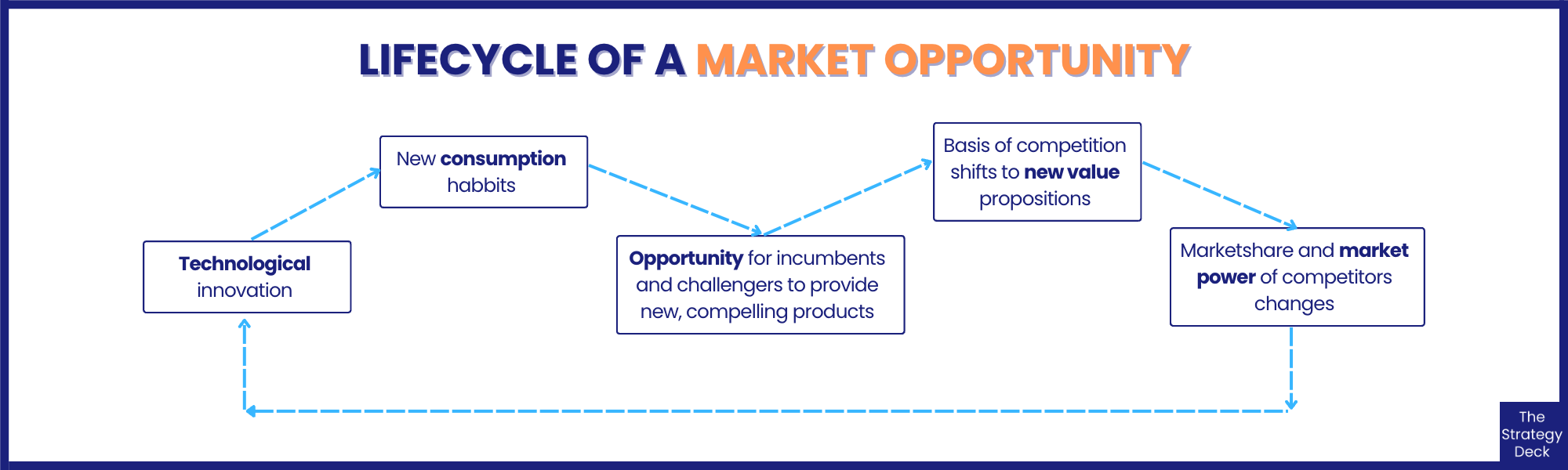

Market transformations happen at multiple levels of the value chain and when they do, they drive changes in consumer habits, at the product level and in the marketshare and market power of competitors in an industry.

End-users, either consumers or enterprise, change their usage patterns, usually enabled by a new technology. As consumption habits change, opportunities open up for incumbents and challengers to provide compelling products to support the new use cases. The basis of competition shifts from the old value propositions to new ones and established players need to overcome the innovator's dilemma to protect and grow their marketshare before nimble, innovative challengers capture the opportunity.

Market transformations are what open up and close windows of opportunity and they have long-lasting effects on the structure of an industry. Some of these effects are diversification and fragmentation of the space, or, on the contrary, consolidation among competitors.

Every time a market goes through this cycle - tech innovation to availability of new kinds of products and value propositions to changes in the market power of competitors - we say that the structure of the market has changed.

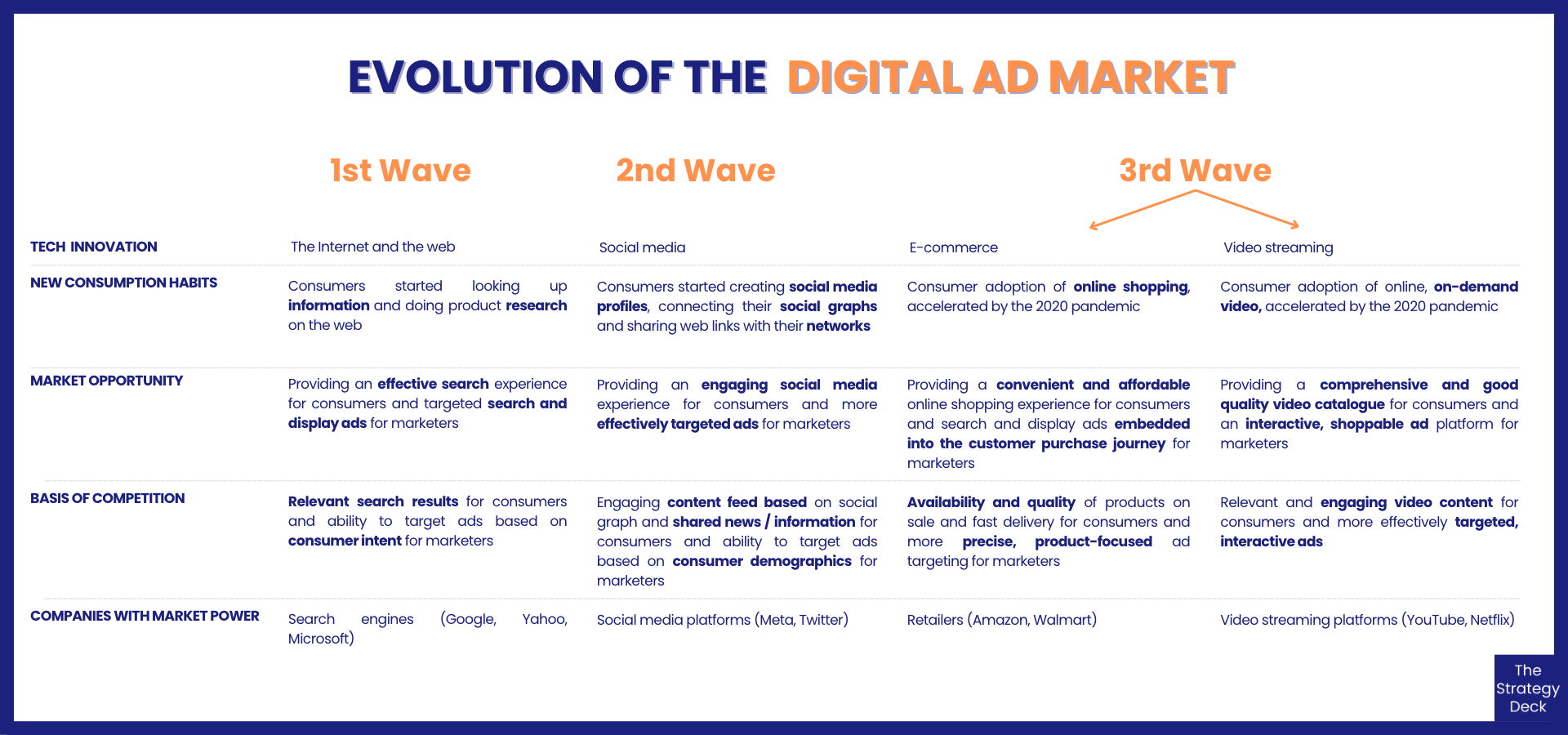

Such a transformation is happening in the digital ad market, where a third wave of ad products, enabled by growth in e-commerce and video streaming, is driving shifts in the marketshare of the incumbents Google and Meta. Challengers, represented by online retailers and video streaming platforms, are providing new ad products and gaining marketshare. In 2022, the digital ad market represented a $500 bn opportunity worldwide, excluding China, with $300 bn of that spent in the US, according to Omdia Research.

But how did it get like that?

1st wave: Search

Driven by consumer adoption of the Internet and the web, search ads were the first major breakthrough in online ads. Whether for information and education or to look up potential purchases, every search is an opportunity for search result and display ads. For consumers, the value proposition revolves around relevant and fast answers and marketers rely on information about the consumer's intent when doing the search to target the ads.

2nd wave: Social Media

Social media platforms allow consumers to create a profile, connect their real-life networks and share news ad videos with their social graph. This shifted the basis for competition for the ad market to providing engaging content feeds to consumers and allowed more effective ad targeting through demographics.

3rd wave: e-commerce and video streaming

The third wave includes two opportunities:

Growth of e-commerce and display ads embedded in the customer purchase journey

Consumer shift from linear TV to video streaming platforms and interactive, shoppable ads

E-commerce retailers are now in a position where they can offer more compelling ad platforms because they have first-party consumer data that spans information about both demographics and purchase history. In addition, ad effectiveness is greater and more easily measured due to its embedding closer to the point of purchase.

Large and medium-sized retailers are the major beneficiaries of this shift and are building digital advertising arms and investing in positioning themselves as compelling ad venues for consumer brands. This move also helps them retain a direct relationship with their customers, without being disintermediated by social media platforms.

Amazon is well underway to leveraging the opportunity - in Q3 2022 its ad network generated $9.5 billion, up 25% YoY. Walmart's media solution operates as Connect in the US and as Flipkart Ads in India.

In the video space, a new ad product in the form of direct-response formats, including shoppable ads, is offering digital streaming providers the opportunity to build ad networks and add to their revenue streams.

The global connected TV advertising market is expected to grow through 2026, tripling in value to reach US $56 bn, according to Omdia Research. YouTube has already rolled out mobile shoppable video ad units and is adding it to connected TVs, but competition is set to increase, with Netflix and Amazon Video developing their video ad networks.

Adtech companies can help medium-sized and, especially, smaller players, connect and operate together their own ad networks and carve out marketshare for themselves.

It is exciting to see changes and innovation in a very important part of the tech market alongside more competition (due to increasing fragmentation), as well as the potential for better products to take over, which will hopefully significantly address current consumer concerns, such as privacy and responsible use of customer data.